As interest rates trend upward, some homebuyers and homesellers are investigating their options on possible ‘workarounds’ to maximize their position in this more challenging environment.

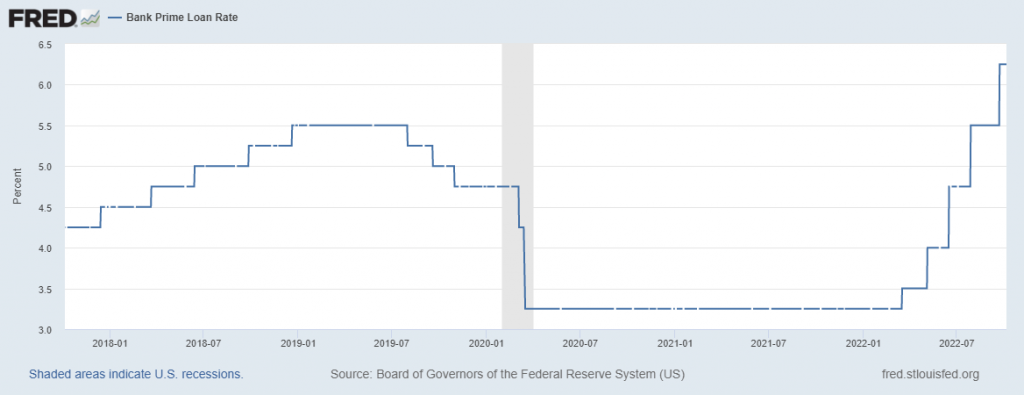

The above graph shows the Federal Reserve’s prime loan interest rate climb. Rates to borrow money have increased significantly in less than a year. While the Federal Reserve interest rate doesn’t identically match consumer interest rates, it’s what banks pay to borrow money, so the prime rate generally reflects the overall mortgage rate trend. The more the Fed Rate rises, the more expensive it is to get a loan.

Why Does It Matter?

The rate homebuyers pay for a home loan has increased. As a result, the overall monthly house payment for new loans has gone up, too. Rising interest rates mean homebuyers qualify for a lower priced home now compared to one year ago. Yet there is indeed a workaround and it’s called owner financing. Perhaps best of all, under certain circumstances, owner financing can benefit both homebuyers and homesellers.

What Is Owner Financing?

Owner financing goes by many names. It’s also called seller financing, seller terms, owner carry, seller carryback and seller carry. A typical owner financing scenario is when a homebuyer purchases property by making an initial down payment to the seller, then continues with additional periodic payments. The payments are often monthly, or some other pre-agreed schedule of loan repayment. While Oregon law has rules in place especially to regulate large-scale property sellers who handle a significant amount of owner-financed transactions (notably commercial firms, such as private finance companies), the process still remains relatively simple for typical Oregon home buyers and sellers who enter into a home sale without using a traditional lender.

What Makes Owner Financing so Powerful

Seller financing may sound ‘blah’ to some, but it can be very powerful to buyers and sellers, because it can:

- Make an otherwise ‘hard to sell’ property more sellable, and/or

- Render an otherwise ‘unqualified’ buyer qualified, whilst escaping considerable loan fees, underwriting and requirements, like an appraisal, and/or

- Provide income to a home seller, with interest, all secured with the protection of a legal instrument in case of default, and/or

- Allow a homebuyer the ability to purchase a home as they sell a less liquid (hard to sell) asset, or re-build credit, and/or

- Give both buyer and seller the flexibility to negotiate what works for them, rather than a bank’s pre-determined, ‘cookie-cutter’ loan term, interest rate, or myriad other conditions.

Practical Benefits

Sellers dislike reducing their price when interest rates rise and make their property less affordable. Conversely, buyers dislike paying those higher interest rates, which make homebuying more expensive. The benefit? Under certain circumstances, buyers and sellers can work together for a ‘win-win’ result using owner financing. It might mean the seller agrees to use owner financing to ‘take payments’ after a significant down payment and not reduce his or her price, while offering the buyer a more attractive interest rate on the remaining balance. Another practical benefit is the usual absence of bank fees, some of which include appraisal, loan, processing and underwriting costs.

What’s The Catch?

A key factor that helps to make seller financing a likely option is if a homeseller has either no loan, or a very small loan remaining on the property they’re selling. Having little or no loan on the home being sold means more of the buyer’s down payment will go to the seller, not diverted to the lender of the seller’s existing home loan. Most home loans now also have what’s called a ‘due on sale’ clause, which means a seller’s existing home loan must be paid off upon the sale of a property. The factor of having no or little loan balance on a property is often the one limiting condition in determining if seller financing is an option. If the property has either no loan, or only a small loan remaining, this can really open the door to seller financing.

Wondering If Seller Financing Is For You?

Contact Roy with Certified Realty for a free consultation to discuss your options, including seller financing. Roy has helped Oregon homebuyers and homesellers since 1988.